Japan’s economic security policy is moving beyond supply chain support and into a more operational phase of institutional implementation. The shift now brings together Foreign Exchange and Foreign Trade Act (FEFTA)-based inbound investment screening, prevention of technology and information leakage, protection of critical infrastructure, support for strategic overseas projects, and stronger intelligence coordination at the center of government. Ongoing Diet deliberations point in the same direction.

The 2026 bill to amend the Economic Security Promotion Act is expected to expand Japan’s economic security framework to include services essential to critical goods, healthcare-related infrastructure, overseas strategic projects and stronger policy-analysis functions. This does not mean that Japan is closing its market. Rather, Japan is moving toward “selective openness”: continuing to welcome investment and business expansion while applying closer scrutiny to technologies, data, ownership structures, governance rights, and supply-chain risks that may affect national-security interests.

For companies and investors, regulatory compliance alone will no longer be sufficient. Businesses will need to explain not only whether a filing is required, but also how their technologies, capital structure, data, customer relationships, procurement networks, and post-transaction governance may be viewed by authorities and partners from a national security perspective. Economic security is therefore becoming a management-level issue that should be considered early in:

- Investment planning and M&A strategy

- Supply-chain design and data governance

- Cross-border partnerships

Companies that can identify security-related risks early, design credible mitigation measures, and communicate their approach clearly will be better positioned to navigate Japan’s evolving policy environment and build long-term trust with regulators, business partners, investors, and customers.

Structural Shift: The Economic Security Promotion Act and Response to Economic Coercion

Japan’s economic security policy is moving beyond its initial focus on critical goods and supply-chain resilience. It is entering a more integrated phase of institutional implementation that includes inbound investment screening, prevention of technology leakage, protection of critical infrastructure, and the strengthening of intelligence capabilities. In 2021, the Kishida administration convened the Economic Security Promotion Council, followed by the enactment of the Economic Security Promotion Act in 2022. The Act established the foundation of Japan’s economic security policy through four pillars:

- securing stable supplies of critical goods

- ensuring the stable provision of critical infrastructure services

- supporting the development of advanced critical technologies

- introducing a non-disclosure system for sensitive patent applications.

Building on this foundation, Japan is now adding more effective mechanisms for risk management. The 2026 bill to amend FEFTA positions the promotion of inbound direct investment as an important policy priority, while also emphasizing the need to address investments that could harm national security, as security concerns increasingly extend into the economic domain. This indicates that Japan is not moving toward a closed approach to foreign investment. Rather, it is seeking to continue accepting investment while more precisely assessing substantive control structures, access to technologies and information, and potential impacts on supply chains.

Alongside these developments, Japan is also moving to strengthen its national intelligence capabilities as a foundation for more effective institutional implementation. The bill to establish the National Intelligence Council would create a body within the Cabinet to deliberate on important matters related to information collection and analysis activities that support key national policy decisions. The government also plans to establish the National Intelligence Bureau as the secretariat of the Council, to strengthen the collection, analysis, and overall coordination of information that is currently dispersed across ministries and agencies.

At the same time, the scope of economic security is expanding beyond domestic regulation and defense-related industries to include overseas business, international transport networks, critical infrastructure including healthcare, and policy-analysis functions. The 2026 bill to amend the Economic Security Promotion Act, which passed the House of Representatives on May 19, 2026 and was sent to the House of Councillors, includes support for overseas projects that contribute to the resilience of international transport networks, new provisions related to services essential to the supply of designated critical goods, the addition of healthcare to the critical infrastructure framework, and the strengthening of research and analysis on economic measures related to national security. As a result, economic security is expanding from a policy focused mainly on protection to one that also supports Japanese companies’ overseas expansion and the development of resilient supply chains.

This shift means that Japan’s economic security policy is no longer only a matter of domestic institutional design. It has become a theme that directly affects the decision-making of global companies and investors. In future inbound investment and M&A transactions in Japan, price and growth potential will not be the only factors that matter. Technologies, data, supply chains, and post-acquisition control structures will increasingly influence whether a transaction is considered viable from a national security perspective. For companies, regulatory compliance alone will not be sufficient. They will need to be able to explain their risk mitigation approach to technologies, capital structure, data, and business relationship that may be viewed as security-related risks by authorities and partners.

Investment Screening Reform: Amendments to FEFTA and Japan-style CFIUS

FEFTA remains the legal foundation of Japan’s foreign-investment review system. Unlike the Committee on Foreign Investment in the United States, or CFIUS model, which is built around a smaller number of deeper case reviews, Japan’s system already operates as a broad front-end screening regime. In fiscal year 2024, the Ministry of Finance (MOF) recorded 2,903 prior notifications for inward direct investment and related transactions. Around 79% of those filings were screened within 14 calendar days, and the average review period was 8.2 business days. At the same time, the system is not merely procedural: withdrawals, non-notified cases, administrative dialogue, and refiling are already important parts of how the regime works in practice.

The 2026 FEFTA amendment bill would make that regime more explicitly national-security-oriented. The MOF’s Japanese bill summary frames the reform around two objectives: continuing to promote sound inward direct investment while responding to the rapid expansion of security concerns into the economic domain. The bill would bring into scope certain indirect acquisitions, where a foreign investor acquires 50% or more of the voting rights in a foreign entity that itself holds covered shares in a Japanese company. It would also require investors to notify proposed risk-mitigation measures relating to national security, and to notify changes to those measures. In addition, the bill would deem certain nominee or contractual arrangements to be transactions by foreign investors, strengthen reporting and possible disposal-related measures for high-risk non-notified transactions, and require the Minister of Finance and the competent business minister to seek opinions from the heads of relevant administrative organs where necessary during screening.

This is the most concrete basis for the growing “Japan-style CFIUS” discussion. The phrase is useful shorthand, but it should not be read to mean that Japan is copying the United States wholesale. The official bill materials do not create a new statutory CFIUS-equivalent committee. Instead, Japan appears to be moving toward a more CFIUS-like operating model within FEFTA framework: more attention to control and beneficial ownership, more focus on mitigation, more interagency consultation, and greater sensitivity to indirect acquisition structures. This direction is also consistent with recent changes that expanded FEFTA core sectors and tightened the exemption framework for certain investors, reflecting greater concern over supply chain protection, technology leakage, military diversion risk and investor attributes.

The practical effect is that FEFTA review is becoming less of a box-checking exercise and more of a national security assessment. The government’s published screening factors already show that authorities consider whether an investment could affect production or technology bases relevant to national security; whether technologies or sensitive information could be leaked or misused; whether supply conditions, stability or quality could be affected; and whether the investor’s capital structure, beneficial ownership, business relationships, foreign-government influence, or compliance history create risk. They also look at the specific rights the investor may exercise after closing, including board or auditor appointments, access to non-public technical or systems information, participation in management committees, and proposals that impose deadlines or pressure on management.

For companies and investors, this means the key question is no longer only whether a filing is technically required. It is whether the transaction can be explained credibly from a national security perspective. Low-risk filings may continue to move quickly, as the fiscal year 2024 timing data suggest, but transactions involving control, dual-use technology, sensitive data, critical supply chains, defense-linked customers, or opaque ownership structures are likely to face a more searching review. The parties should therefore prepare a security narrative early: who ultimately owns and controls the investor; whether any foreign-government influence exists; what information and technology the investor will access; how data and sensitive know-how will be ring-fenced; how supply continuity will be protected; and what governance rights the investor actually needs. In this sense, “Japan-style CFIUS” is best understood not as a new institution, but as a gradual hardening and sophistication of Japan’s existing FEFTA system.

Case Study: Implications of the Makino Milling Machine Case

The Makino Milling Machine case shows what Japan’s more security-conscious investment screening environment can look like in practice. On April 23, 2026, the Finance Minister confirmed that the government had issued a recommendation to discontinue MBK Partners’ planned acquisition of Makino under FEFTA. MBK Partners is a South Korea-based private equity firm founded by Korean-born American investor Michael B. Kim, with a dedicated focus on investments in North Asia.

The government’s concern was not simply foreign ownership in the abstract. It focused on Makino’s position in Japan’s defense-relevant manufacturing ecosystem, including:

- its role as a world-class machine-tool manufacturer

- the use of its products by Japanese defense-equipment manufacturers

- the risk of technology or information leakage affecting production bases relevant to national security

The recommendation followed review by the MOF and the Ministry of Economy, Trade and Industry (METI) through the relevant FEFTA process.

Company-side disclosures indicate that mitigation was proposed but did not resolve the authorities’ concerns. MM Holdings, the MBK Partners-related tender offeror, stated that it had spent approximately ten months engaging with Japanese authorities and had proposed risk-mitigation measures while referring to recent CFIUS practice in the United States. Nevertheless, on April 30, 2026, MM Holdings accepted the recommendation, terminated the tender offer agreement with Makino, and decided not to commence the tender offer. The disclosure also referred to information that may not be sensitive on its own but could become sensitive from a national security perspective when combined with other information. This “mosaic” logic suggests that Japanese authorities may focus not only on obvious defense secrets, but also on industrial, technical, procurement, and customer-related information that becomes strategically meaningful when aggregated.

The case is important because mitigation did not save the deal. It shows that Japan’s review is not limited to identifying whether a transaction falls into a sensitive sector. The state may also assess whether proposed mitigation is operationally credible, whether it is compatible with the investor’s intended post-acquisition role, and whether the investor can realistically pursue its value-creation plan without accessing the very information the government wants to protect. Makino also demonstrates that Japan’s historical preference for quiet risk management has limits: where the target is embedded in defense-relevant production, advanced manufacturing or sensitive technology ecosystems, and information access concerns cannot be resolved, the government is prepared to use formal discontinuance powers.

At the same time, Makino should not be over-read as a sign of broad investment closure. It should be read alongside MBK’s reported acquisition of Altemira Holdings, an aluminum business group, which appears to have received FEFTA clearance. Press reports indicate that Altemira also had an economic-security nexus because it handles certain lithium-ion battery-related materials, but the transaction was reportedly cleared through Japan’s prior screening process. The contrast suggests that the issue is not simply whether a company falls within a core sector. Rather, the key factors appear to include the sensitivity of the target’s technologies, its relationship to defense production, the information-access risk created by full ownership, and the credibility of mitigation.

For businesses, the combined lesson from Makino and Altemira is not that foreign capital is unwelcome. Japan still appears to be pursuing “selective openness" rather than blanket restriction. Transactions involving defense-adjacent manufacturing, dual-use technologies, sensitive data, critical infrastructure or hard-to-ring-fence information access may face intense scrutiny, while transactions with a core-sector connection but lower leakage or defense-production risk may still be cleared. For multinational investors, the strategic question is therefore not only “Is this a core sector?” but “How will the Japanese state understand this target’s technologies, data, customers, supply-chain role and post-acquisition governance from a national security perspective?”

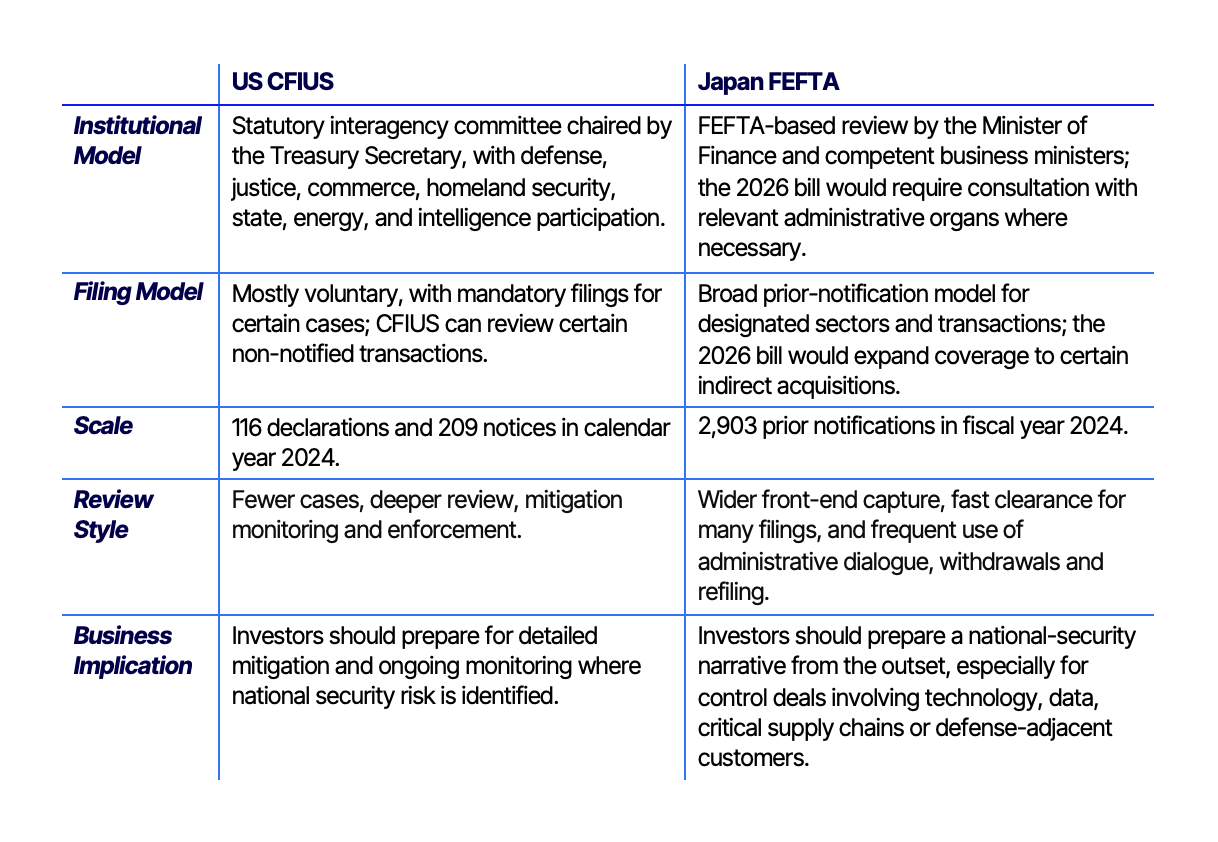

Global Benchmark: Comparison with US CFIUS

The United States remains the most relevant benchmark for understanding where Japan’s regime may be heading, even though the two systems are structurally different. US CFIUS is a Treasury-chaired interagency committee that reviews certain foreign-investment and real-estate transactions for national security risk.

The US process is deeper and more discretionary than Japan’s broad prior-notification model. CFIUS filings are generally voluntary, although certain transactions are subject to mandatory filing requirements. Parties may submit a shorter declaration or a full notice, with higher-risk cases potentially moving into investigation, mitigation, or presidential review. If CFIUS clears a transaction, the parties ordinarily receive “safe harbor,” meaning CFIUS will not later reopen the transaction unless certain limited conditions apply, such as false or misleading information.

The 2024 CFIUS data illustrate this narrower-but-deeper model. CFIUS assessed 116 declarations and reviewed 209 notices, moving more than half of the notices into investigation and adopting mitigation measures or conditions in relation to 25 notices. It also monitored 242 mitigation agreements and conditions and conducted 79 site visits, showing the importance of post-clearance monitoring and enforcement.

Japan’s FEFTA system, by contrast, still screens much more widely at the front end. Japan recorded 2,903 prior notifications in fiscal year 2024, compared with CFIUS’s 325 total declarations and notices in calendar year 2024. Most Japanese filings cleared quickly, while the US system devoted more resources to investigations, mitigation monitoring, site visits and enforcement. The difference is therefore not simply that one system is “stricter” and the other is “lighter.” The US model is narrower but deeper; Japan’s model is broader and more administrative.

The 2026 FEFTA amendment bill would narrow that gap, but it would not erase the basic difference. Japan would still not have a US-style CFIUS committee. However, the bill would move Japan closer to a risk-weighted, mitigation-conscious and interagency model by requiring notification of national-security mitigation measures, covering certain indirect acquisition structures, and requiring consultation with heads of relevant administrative organs where necessary. In practical terms, Japan may remain fast for routine filings but become more demanding for transactions involving control, sensitive technologies, defense-linked production, critical infrastructure, strategic supply chains, or foreign-government influence.

For companies, the comparison with CFIUS is useful because it shows the likely direction of travel. Investment screening should not be treated as a narrow legal filing exercise. Investors should prepare evidence on ultimate ownership, beneficial control, foreign-government exposure, governance rights, information access, technology controls, data ring-fencing, supply continuity and compliance monitoring. The key implication is that Japan may increasingly expect mitigation thinking to be built into transaction design from the outset.

Differences at a Glance

Beyond CFIUS: Amendments to the Economic Security Promotion Act and Expansion of Policy Scope

Alongside FEFTA reform, Japan is also pursuing broader measures to strengthen economic security. The Diet is currently deliberating a bill to amend the Economic Security Promotion Act, the country’s core economic security legislation enacted in 2022. The amendment bill should be understood as a significant expansion of the scope and tools of Japan’s economic security policy, covering critical goods, critical infrastructure, critical technologies, overseas business activities, and policy-analysis capabilities. In other words, Japan’s economic security policy is evolving from supply-chain protection toward a more integrated approach that combines investment screening, technology-leakage prevention, infrastructure protection, overseas strategic finance, and policy intelligence.

The original Economic Security Promotion Act created four main pillars: securing the stable supply of designated critical goods, including semiconductors, batteries, critical minerals, machine tools, industrial robots and cloud programs; protecting critical infrastructure services; supporting the development of critical technologies; and establishing a system to keep certain sensitive patent applications undisclosed. The amendment bill would expand this framework in three main ways. First, it would allow the government to support services that are indispensable to the supply of designated critical goods, reflecting a broader understanding of supply-chain resilience that includes logistics, production, maintenance, and other enabling functions. Second, it would add the medical sector, including certain hospitals and medical digital transformation-related functions, to the critical infrastructure framework. Third, it would broaden the range of public research funds that can be used to support designated critical technologies.

One of the most notable features of the bill is the creation of a new framework for “designated overseas projects” that are important to Japan’s economic security. These projects are defined broadly to include overseas facilities and operations that strengthen international transport networks, support the provision of important services, or enable the overseas deployment of important technologies. Private companies would be able to submit plans for such projects, obtain ministerial certification, and receive support from the government and the Japan Bank for International Cooperation (JBIC). The amendment would also enable JBIC to take on greater risk for certified economic security projects, with the aim of mobilizing private capital.

This is a significant shift, although the bill itself does not list specific industries, related government strategy discussions point to areas such as semiconductors, drones and other unmanned systems, shipbuilding, critical minerals and materials, and port and logistics infrastructure. The policy logic is that Japan wants to help its companies build supply chains and strategic business footholds in countries that are less vulnerable to economic coercion or geopolitical disruption. Japanese companies’ overseas expansion is therefore being reframed not only as commercial activity, but also as part of national resilience and security policy.

The bill also seeks to strengthen Japan’s ability to analyze and anticipate economic security risks during peacetime. It would create a comprehensive economic security think tank function through the Research Institute of Economy, Trade and Industry (RIETI), a policy research institute associated with METI. The aim is to build stronger capabilities for research, analysis, and policy recommendations across diplomacy, intelligence, defense, economics, and technology. In parallel, the bill would establish a statutory public-private council to promote structured information sharing and consultation between government and industry, with confidentiality obligations designed to enable more substantive exchanges on sensitive risks.

For global businesses, the key implication is that Japan’s economic security policy is becoming more integrated and more proactive. The amendment bill points to a model in which the state not only reviews or restricts risky transactions, but also supports critical industries, protects essential infrastructure, finances strategic overseas projects, and builds permanent analytical capacity. Japan’s economic security agenda is therefore shifting from defensive screening toward a more comprehensive system for shaping markets, supply chains, and corporate behavior in line with national security priorities.

Implications for Business

As economic security becomes a more central factor in Japan’s policy environment, Japanese companies, foreign companies, and investors will all need to incorporate national security considerations into transaction planning and business strategy. Sensitive technologies, critical supply chains, data protection, dual-use risks, and foreign-ownership structures can no longer be treated simply as legal or compliance matters to be reviewed at the final stage of a transaction. They are becoming board- and management-level issues that should be considered early in strategic decision-making.

For Japanese companies, building internal structures to manage economic security risks will become increasingly important. Economic security cuts across corporate governance, investment review, research and development (R&D) strategy, procurement, supply chain management, and crisis preparedness. For example, Mitsubishi Electric has established an Economic Security Management Office and developed a group-wide framework to coordinate economic security functions across business units and domestic and overseas affiliates. This kind of approach shows that economic security is becoming a cross-functional management issue involving legal, public affairs, technology, procurement, business development, and senior management teams.

Foreign companies and investors will also need to adjust their approach to Japan-related investments and partnerships. Where a target business involves sensitive sectors or critical technologies, they should identify economic security issues at an early stage, consider prior consultation with relevant authorities where appropriate, and prepare risk mitigation measures. These may include restrictions on access to sensitive information, governance safeguards, commitments on domestic supply, cybersecurity measures, and contractual arrangements to protect critical technologies and data. In this environment, formal compliance with filing requirements may not be sufficient to address broader economic security concerns.

The implications are particularly important in three areas:

Defense and Technology

Defense and technology risks are no longer limited to traditional defense equipment. They also include dual-use technologies such as semiconductors, AI, quantum, space, cybersecurity, robotics, drones, and advanced materials. Companies need to assess whether their technologies could have security-related applications, and whether foreign investment, partnerships, or data-sharing arrangements could create risks of technology leakage or access to sensitive information.

Healthcare

Healthcare is becoming part of the economic security agenda because medical resilience is now treated as national resilience. Relevant areas include pharmaceuticals, vaccines, medical devices, diagnostics, biotechnology, digital health, and medical data. The pandemic demonstrated that medical supply chains, domestic production capacity, infectious disease preparedness, patient data protection, and the cybersecurity of healthcare systems are directly linked to national resilience.

Critical Minerals

Critical minerals are a strategic vulnerability for Japan because of its dependence on imported resources. Relevant areas include rare earths, battery materials, semiconductor-related materials, and minerals used in renewable energy technologies. Given Japan’s dependence on imported resources, companies need to assess not only price and availability, but also supply concentration, country risk, export controls, sanctions exposure, transport routes, and alternative sources of supply.

Overall, economic security is moving from the margins of legal and regulatory compliance to the core of corporate strategy. Companies will need to treat economic security not as a one-off regulatory hurdle, but as an ongoing management capability that shapes:

- Investment decisions

- Partnership structures

- Supply chain design

- Data governance

- Stakeholder engagement

Those that identify risks early, develop credible mitigation measures, and communicate their approach clearly will be better positioned to complete transactions smoothly, maintain trust, and demonstrate long-term reliability and resilience in Japan.

This document was developed as deep insight on strengthening Japan's intelligence and economic security. For additional information, reach out to Yuichi.Kori@edelman.com